I was looking for a shorthand way of summarising what I thought were the main political risks that are in the minds of investors in South African financial markets.

Note that the emphasis here (in what appears below) is what I think is an appropriate prism for investors in financial markets, and specifically those with an horizon of a maximum of 5-7 years.

If I was looking at broader security issues, particularly with regard to the stability of the state and ruling party, I would have had a significantly different emphasis – and have aspects that are both more negative and more positive than that which appears below. Hopefully, at some time in the future, I will post here a more general threat or risk analysis that would be of more specific relevance to South Africans who hope to live and work here.

Finally, before I get on with it, I do not explore the potential for an upside suprise here … but there does appear to me to be a slight accumulation of good news, albeit against a dark background.

SA Politics and financial markets – 3 risks

- Unpredictable and/or negative government economic policy interventions: Medium seriousness. Medium likelihood. Short- and medium-term duration (next few months to five years);

- Escalating social unrest – perhaps leading to “Arab Spring” type event: Very serious. Very unlikely. Medium- to-long duration (five to seven years);

- Ratings downgrades and tension between ambitious government plans and narrowing fiscal space: Serious risk. Medium likelihood. Short- and medium-term duration (one to three years).

Unpredictable and/or negative government economic policy interventions

Medium seriousness. Medium likelihood. Short- and medium-term duration (next few months to five years)

What it’s about: Most obvious are new interventions in the mineral and exploration sectors (including new taxes, price setting, beneficiation requirements, export restrictions, uncertainty about licence conditions and significantly increased ministerial discretion via the Mineral and Petroleum Resources Amendment Bill), but there are comparable interventions across the economy, as indicated in the ANC’s Mangaung Resolution and in a range of proposed regulatory and legislative changes, including those relating to telecommunications, liquid fuels, the labour market, employment equity and Black Economic Empowerment (to name just a few).

My view: Since 1994, it has generally been the case that markets consistently overestimate the risk that the ANC and its government will take significantly populist policy measures. The best example of this was in July 2002, when exaggerated targets for black equity participation in the mining sector where leaked and R52b left the JSE resources sector in 72 hours – a buying opportunity of note. However, the traction Julius Malema was able to achieve with disaffected youth post-2009 and the implicit defection from the ANC and its allies in the platinum strikes last year have catapulted the ANC into something of a policy scrabble. While nationalisation is off the agenda, it has been replaced by a policy push that hopes to deploy private companies, through regulation and other forms of pressure, to achieve government (and party) targets of employment, revenue generation, service delivery to local communities and infrastructure build. Increases in the tax take look likely – it’s purely a question of ‘how much the market can bear’.

Government intervention, per se, is less the issue here but rather the confused, generalised and uncertain nature and intent of the interventions. If the interventions do not have the desired results (growth, employment and equality), the risk is that government does not reassess the wisdom of the intervention, but instead uses a heavier hand.

Financial markets: Policy uncertainty puts downward pressure on investment, employment and output in all sectors. In South Africa, these negative impacts will be felt most keenly by companies most exposed to government licencing and regulatory power, or most exposed to government’s political prioritisation. Resources, telecommunications and agriculture all fall into one, or both, of these categories.

Escalating social unrest – perhaps leading to “Arab Spring” type event

Very serious. Very unlikely. Medium-to-long duration (five to seven years).

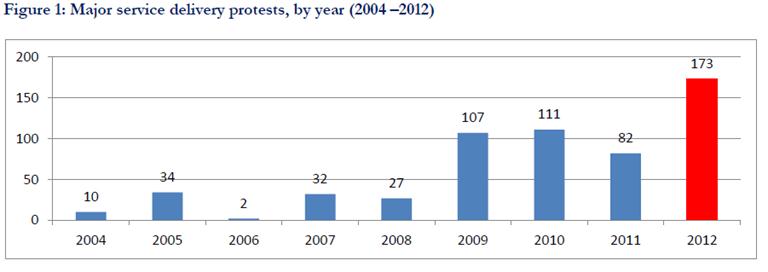

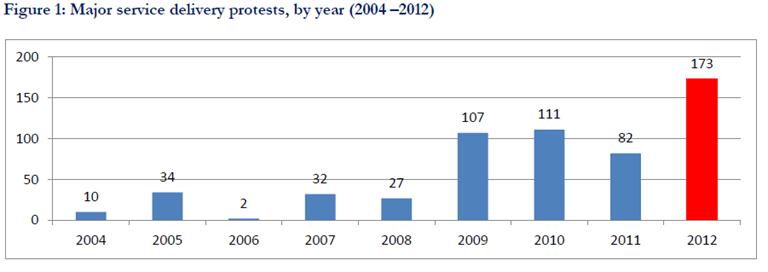

What it’s about: Significant and consistent (apparently linear) growth in service delivery protests, combined with growing levels of industrial unrest (in 2012, anyway) seem to imply that such unrest could continue to escalate until it reaches a point of ‘phase state change’ (as in thermodynamics, referring to changing states of matter – to/from solid, liquid and gas). Thus, the risk is of a sudden systemic shift from unstable to revolutionary/insurrectionary.

My view: Increasing protest and industrial unrest are normal – and fairly consistent – features of South African political life and have been since at least the mid-1970s. Even before 1994 there was no real expectation that unrest would lead naturally to insurrection. A rapid phase state change, like an Arab-spring type event, requires (perhaps indirectly) contesting political formations and ideologies as well as the widespread failure – or absence – of social institutions (parliaments, courts) that direct, mediate and give expression to grievances and/or conflicting group interests. South Africa is rich in such institutions and there is no evidence that large groups of dissenting voices have permanently failed to find expression in society’s normal processes and institutions – even when some of those processes include robust forms of public dispute. However, South Africa does have some comparable features to countries that have had ‘Tunisia-moments’ – including high and growing youth unemployment, high levels of visible inequality and serious government corruption – so we would keep an eye on the escalating ‘service delivery protest’ trends, as evidenced in graphs from Municipal IQ below.

Industrial relations unrest is slightly different from – and more negative than – the question of social unrest as a whole. Trade unions are strong and growing in South Africa, and contestation between them is vigorous, even violent – as we saw in the platinum sector in 2012. Trade unions are businesses with an enticing annuity income flow – and this will drive their contestation. The collective bargaining system in South Africa is functioning sub-optimally for a number of reasons – including inappropriately high levels at which automatic recognition kicks in – and the disarray in the system also drives unrest. This conjunction of subjective and objective conditions means I am less sanguine about industrial relations stability (than about stability per se) and expect this to remain a negative investment feature for the next several years. I am specifically negative on public sector industrial relations stability for 2013.

Thus, I do not think unrest and social discord will lead to any radical policy or political discontinuities, but will remain a constant drain on confidence. I also think this phenomenon will tempt government into keeping spending (on the public sector wage bill and on social grants) at above-inflation levels – helping to feed uncertainty and unpredictability in state finances, inflation, the currency and the bond markets.

Additionally, I think labour unrest will remain a seriously destabilising factor of production – including via disruption of services in public sector strikes.

Financial markets:

Resources, agriculture and construction are most exposed through their reliance on large, aggregated and often low-skilled/low-pay labour forces. The financial services and retail are less exposed to (but not immune to) the negative effects of industrial action.

Ratings downgrades and tension between ambitious government plans and narrowing fiscal space

Serious risk. Medium-likelihood. Short- and medium-term duration (one to three years).

What it’s about: The ruling party is facing something of its own ‘fiscal cliff’. The ANC feels itself in danger of losing some support because of failure to deliver employment growth or adequate reductions in poverty and inequality. Foreign investors agree this is a risk, but will not necessarily agree to fund the gap. This tension is among the reasons that all three major rating agencies (Moody’s, Fitch and S&P) downgraded SA’s sovereign rating in 2012 (Fitch in January this year) and both Moody’s and S&P put SA on watch list for future downgrades. The ANC secures political support, at least in part, through spending on the public sector wage bill and on social grants – which together now make up more than half of annual non-interest government spending. Additionally, the ANC has occasionally shown itself hostage to the views of its alliance partners or popular opinion in its spending and revenue plans (Gauteng toll-roads, youth wage subsidy). The ratings agencies don’t like the tension and I expect the bond markets won’t either.

My view: South Africa maintains respectable debt-to-GDP ratios, although these grew to 39% of GDP by end-2012, substantially higher than the 34% for emerging and developing economies as a whole. When Fitch downgraded SA earlier this year, it specifically mentioned concerns about SA’s rising debt-to-GDP ratio, given that the ratio is higher (and rising at a faster pace) than the country’s peers.

South Africa is uniquely (eg in relation to its BRICS peers) exposed to foreign investor sentiment through the deficit on the current account combined with liquid and deep fixed interest markets. SA’s widening deficit on the current account is a specific factor that concerns the rating agencies and is one of the metrics the agencies will use to assess SA’s sovereign risk in the near future. Further downgrades are the risk – potentially driven by foreign investor sentiment about political risks. Non-investment grade (junk bond status) is not an inconceivable future rating.

Financial markets: A significant sell-off in the rand, coupled with persistent currency volatility and reduced foreign capital inflows. Traditionally this scenario would mean investors look for rand hedges and attempt to get exposure to export-orientated sectors, including manufacturing – and to stay out of the bond market. Offshore borrowing costs will be raised for domestic companies – as well as for the country as a whole. This risk has an internal feedback loop (downgrades make debt more difficult to pay, leading to further downgrades) and naturally feeds other political risks, including in relation to taxation, clumsy government intervention, social stability and property rights.